Every day, thousands of traders watch the best memecoins skyrocket while they sit on the sidelines, wondering how others spotted the opportunity first. The secret isn't luck or insider knowledge; it is the most profitable Crypto trading strategy used by modern pros: OnChain analytics. This skill lets you read blockchain data like a map, showing where smart money flows before prices explode. This article breaks down OnChain metrics, wallet tracking, and transaction patterns so you can identify emerging trends and understand what separates profitable trades from costly mistakes.

Learning to interpret blockchain data transforms how you approach markets, giving you the foundation to develop strategies that actually work instead of chasing hype. While human intuition identifies the “why,” an AI Crypto trading bot handles the “when” and “how” with tireless efficiency.

Summary

- OnChain analytics transforms Crypto trading from reactive guessing into evidence-based decision-making by revealing where smart money flows before price movements occur. Reading blockchain data, wallet-tracking patterns, and transaction volumes provides the foundation for identifying emerging trends that separate early, profitable entries from late, chasing behavior that leads to losses.

- The search for a single universally profitable trading strategy fails because market conditions constantly shift between trending, ranging, volatile, and quiet regimes. A breakout system that captures explosive gains during trending markets generates repeated false signals and small losses during sideways consolidation.

- Position sizing determines survival more than entry accuracy, as a trader with 60% win rate can still destroy their account by risking 20% per trade. Three consecutive 20% losses reduce a $10,000 account to $5,120, requiring a 95% gain just to break even.

- Professional traders backtest strategies across at least 3 years of historical data to capture different volatility regimes and liquidity conditions, with 78% of institutional traders using forward testing for 3-6 months before deploying real capital. This validation process exposes how real-time price formation, actual spreads, and execution delays differ from historical simulations, revealing performance decay that often cuts theoretical edge in half once slippage and timing costs enter the equation.

- Emotional override breaks even objectively profitable strategies, as research on Prospect Theory shows people feel losses roughly twice as intensely as equivalent gains. After three consecutive losses, traders abandon rules that looked clear during calm markets and begin skipping signals or modifying position sizes exactly when the strategy needs consistent execution to demonstrate its statistical characteristics across many trades.

Coincidence AI’s AI Crypto trading bot consolidates on-chain positioning data, advanced wallet tracking, and institutional-grade execution infrastructure into a single, cohesive interface. This integration is designed to compress the discovery-to-deployment cycle, ensuring that your theoretical edge survives the transition into live markets.

Why Everyone is Searching for the Most Profitable Strategy

The search for the single most profitable Crypto trading strategy feels urgent because traders believe clarity equals control. When prices swing 15% in an afternoon, and social feeds overflow with screenshots of 10x returns, the instinct is to find one reliable method and commit to it fully.

The promise is simple:

- Discover the right approach

- Execute it consistently

- The chaos resolves into predictable profit

That promise rarely survives contact with reality.

The Cycle That Keeps Repeating

Traders enter Crypto expecting to find a system that works in all conditions.

- They study trend following until a sideways market erases weeks of gains.

- They switch to scalping, only to watch transaction fees and slippage consume their edge.

- Then they pivot to long-term holding, convinced patience is the answer, until a 40% drawdown tests their conviction and they exit near the bottom.

The pattern is exhausting. After losses, the natural response is to question the strategy rather than the execution or market fit. This creates a cycle where traders hop between methods before any single approach has time to demonstrate its true characteristics. A strategy that might work beautifully in trending markets gets abandoned during consolidation. One designed for volatility gets discarded during steady uptrends.

The Psychology of Recency Bias

Conflicting advice accelerates the confusion. One group insists that algorithmic systems remove emotion. Another swears by discretionary trading and reading market sentiment. Forums highlight massive wins from leverage trading while simultaneously warning that 90% of leveraged traders lose money.

Without a framework for evaluating which advice applies to which context, traders default to recency bias, chasing whatever worked most recently for someone else.

Why Past Performance Misleads

Historical backtests create false confidence. A strategy optimized on 2021 bull-market data might deliver extraordinary returns, but those same parameters often fail when volatility patterns shift or liquidity conditions change.

Crypto markets adapt quickly. What worked during low-interest-rate environments behaves differently when macro conditions tighten. Strategies built around specific token behaviors break when those tokens lose relevance or new narratives emerge.

The Affiliate Bias in Crypto Media

According to Glen Allsopp's analysis of search results, 169 out of 250 “best X software” searches return results dominated by affiliate-driven recommendations rather than evidence-based evaluation. The same dynamic exists in Crypto strategy content. What gets promoted most aggressively often has little correlation with what actually produces consistent returns across different market regimes.

Overfitting is the hidden trap. Building a strategy around patterns that worked in the past creates the illusion of edge without substance. The strategy looks brilliant in hindsight, but lacks robustness going forward because it's tuned to noise rather than signal.

The Expectations That Sabotage Progress

Profitable trading systems rarely deliver smooth equity curves. They include drawdowns, losing streaks, and periods where nothing seems to work. Traders expect constant wins or steady upward progression, but even the best approaches experience extended periods of underperformance.

When reality:

- Doesn't match expectations

- The strategy gets blamed

- The cycle starts again

Identifying Market Regimes

The misconception runs deeper than impatience. Most traders believe profitability comes from discovering the secret method nobody else knows about. The truth is far more practical: edge comes from matching the right approach to current conditions and executing it with discipline.

A simple trend-following system applied consistently in the right environment outperforms a sophisticated strategy used sporadically or in mismatched conditions.

The Liquidity Fragmentation Problem

Traditional trading platforms further fragment this process.

Traders jump between:

- Exchanges to access tokens

- Use separate charting tools

- Rely on Twitter for sentiment

- Manually track wallet movements across blockchain explorers

This scattered workflow makes it nearly impossible to develop the consistent execution that separates profitable traders from those who perpetually search for better methods.

Most platforms stop at showing you the data; Coincidence AI executes on it. Our AI Crypto trading bot engine consolidates OnChain signals, social discovery, and institutional-grade execution into a single conversational agent, removing the friction and hesitation that erode your theoretical edge.

What Actually Determines Success

Market regime matters more than method sophistication. A basic breakout strategy works beautifully in trending markets but bleeds slowly in choppy conditions. Mean reversion approaches profit from range-bound action but get destroyed when genuine trends emerge.

The skill isn't finding the universally best strategy; it's recognizing which environment you're trading and selecting the approach that fits.

Archetypes of Trading Timeframes

Time horizon shapes everything. Scalping requires different infrastructure, psychology, and market conditions than swing trading or long-term accumulation. Mixing time horizons within a single strategy creates internal contradictions, guaranteeing inconsistency.

Risk tolerance isn't just about position sizing. It determines which drawdown profiles you can psychologically withstand. A strategy with 30% drawdowns might be mathematically sound, but if you can't sleep through those periods without panic-selling, the math becomes irrelevant.

Surviving Market Phase Transitions

Discipline separates theoretical edge from realized profit. The best strategy executed poorly loses to a mediocre strategy executed consistently. Most traders never discover this because they switch approaches before experiencing enough market cycles to understand how their chosen method actually behaves across different conditions.

But knowing what makes a strategy work is only half the equation; the harder question is what makes it last when markets inevitably turn against you.

Related Reading

- Crypto Trading Tips

- Are Crypto Trading Bots Profitable

- What Is Long And Short In Crypto Trading

- What Is Swing Trading Crypto

- What Is Wash Trading Crypto

- Crypto Backtesting

- How Does Crypto Leverage Trading Work

- DCA Bot vs Grid Bot

- Forex Crypto Trading

- 30 Second Crypto Trading

What Makes a Trading Strategy Profitable and Sustainable

Sustainability comes from structure, not prediction. A profitable strategy doesn't require accurate forecasting. It needs rules that protect capital when wrong and capture gains when right, applied consistently across enough trades that a statistical edge materializes.

The difference between strategies that survive and those that collapse lies in how they handle the inevitable periods when nothing works.

Clear Entry and Exit Rules

Vague criteria create hesitation. When a trader decides to “buy when momentum looks strong,” they introduce interpretation into a process that demands precision.

- Strong to whom?

- Compared to what timeframe?

- At what confirmation threshold?

Each ambiguous word becomes a decision point where emotion can override logic.

Concrete rules eliminate that friction. A system might specify:

- Enter long when the daily close exceeds the 50-period moving average by at least 2%

- With volume 30% above the 20-day average

- Confirmed by a higher low on the 4-hour chart

The specificity removes doubt. Either conditions are met, or they aren't.

The Chandelier Exit

Exits matter more than most traders realize. According to TradeVision Blog's analysis, 95% of traders lose money, often because they lack systematic exit rules. A strong entry without a defined exit becomes a gamble on hope.

Professional systems include profit targets based on average true range, stop losses tied to support levels or percentage thresholds, and trailing exits that lock in gains as price moves in the trade's favor. These aren't suggestions. They're the guardrails that prevent good trades from turning into regrets.

Risk Management and Position Sizing

Position sizing determines survival. A trader with a 60% win rate can still blow up their account if they risk 20% per trade and hit three consecutive losses. The math is unforgiving. Three 20% losses reduce a $10,000 account to $5,120. Recovery from that drawdown requires a 95% gain just to break even.

Limiting risk per trade to 1-2% of total capital changes the equation entirely. The same three losses reduce the account by only 6%, leaving $9,400 and requiring just a 6.4% gain to recover. This asymmetry between drawdown and recovery is why capital preservation comes before profit maximization in every durable system.

The Drawdown-to-Expectancy Ratio

Win rate alone doesn't predict profitability. A strategy that wins 40% of the time can vastly outperform one with 70% accuracy if the average winner is three times the size of the average loser. The combination of win rate, average gain, and average loss creates expectancy. Positive expectancy across many trades is what separates gambling from systematic trading.

Market Regime Awareness

Strategies break when conditions shift. A breakout system designed for trending markets will trigger repeatedly during choppy consolidation, resulting in small losses on each false signal. After weeks of sideways price action, traders abandon the approach entirely, convinced it doesn't work. Then a genuine trend emerges, and they miss it because they're no longer watching.

Mean-reversion strategies suffer from the opposite problem. They profit beautifully when prices oscillate within a range, buying dips and selling rallies. But when a real breakout occurs, they keep buying as the price falls or selling as it rises, fighting the trend until losses accumulate beyond their tolerance.

Regime-Specific KPI Sets

The critical skill isn't choosing between trend following and mean reversion. It's recognizing which regime currently exists and applying the appropriate method. Some traders use volatility filters, switching strategies when the average true range crosses certain thresholds.

Others monitor price structure, noting whether recent swings create higher highs and higher lows (trending) or oscillate within boundaries (ranging). The specific filter matters less than having one at all.

The 4 Phases of a Crypto Market Cycle

Traditional workflows make regime recognition harder than it needs to be.

- Traders check price charts on one platform

- Pull volatility data from another

- Cross-reference whale wallet movements on a blockchain explorer

- Scan social sentiment on Twitter

By the time they synthesize all inputs, the opportunity has moved.

The Velocity of Information

Coincidence AI surfaces:

- High-fidelity on-chain positioning data

- Breakout signals

- Deep wallet tracking within a single, unified interface

By integrating these critical streams directly with an AI Crypto trading bot, the platform compresses the recognition-to-execution cycle from minutes to seconds.

Statistical Edge Over Many Trades

Individual trades are noise. Aggregate results are a signal. A trader who wins seven out of ten trades this week might lose six out of ten next week. The sample size is too small to distinguish skill from variance.

Over 200 trades, patterns stabilize. Win rates converge toward their true probability. Average gains and losses reveal whether the system actually has an edge or just got lucky during favorable conditions.

Modeling Friction (Slippage and Fees)

Backtesting exposes whether an apparent pattern is statistically meaningful or coincidental. A strategy that shows 15% annual returns over three months of historical data might be curve-fitted to noise. The same strategy tested across five years, including both bull and bear markets, reveals its true robustness. Forward testing on live markets with real execution costs adds another layer of validation that no backtest can replicate.

The gap between theory and execution is where most edge disappears. Slippage, transaction fees, and the psychological difficulty of following rules during losing streaks all erode returns that looked pristine in simulation.

Discipline in Execution

Knowing the rules doesn't mean following them. After three consecutive losses, the temptation to skip the next signal becomes overwhelming. After three consecutive wins, the urge to increase position size “just this once” feels justified. Both impulses destroy consistency.

Variance vs. Strategy Failure

Traders quit strategies during dry periods, mistaking normal variance for strategy failure. One trader described running a systematic approach for months, barely breaking even, ready to abandon it entirely.

Then, a single two-week period captured a major trend move, recovering all previous small losses and generating significant profit. Had they quit during the dry streak, they would have missed the exact conditions their strategy was designed to exploit.

Adapting to Regime Shifts

The strategies that survive aren't necessarily the most sophisticated.

They're the ones traders can actually follow through:

- Drawdowns

- Boredom

- The constant noise of conflicting opinions

A simple system executed with discipline outperforms a complex one applied inconsistently. But even perfect execution of a robust strategy means nothing if the approach itself can't adapt when market structure fundamentally changes.

10 Most Profitable Crypto Trading Strategies (By Market Style)

Profitability in Crypto trading isn't about discovering one dominant method. It's about matching your approach to the specific market conditions you're facing right now. A strategy that captures explosive gains during trending markets will bleed capital in sideways consolidation.

The question isn't which strategy works best universally, but which one aligns with whether prices are:

- Trending

- Ranging

- Volatile

- Quiet

1. Trend Following (Trending Markets)

Trend following captures sustained directional moves without trying to predict when they'll reverse. The approach waits for confirmation that momentum has established itself, using moving averages, trendlines, or momentum filters to verify that a trend is in place before committing capital.

Crypto markets generate powerful multi-week or multi-month trends driven by:

- Narrative shifts

- Liquidity cycles

- Macro sentiment

When these conditions align, trend followers ride the wave rather than fight it. The strategy works when markets show strong directional participation with clear higher highs and higher lows (or lower lows and lower highs in downtrends).

Identifying Market Compression

The failure mode is predictable. Choppy sideways markets trigger false signals repeatedly, generating small losses on each whipsaw. Traders who don't recognize when consolidation has replaced trending will watch their equity curve flatten as the strategy hits conditions it wasn't designed for.

2. Breakout Trading (Volatility Expansion)

Breakout strategies enter when:

- Price escapes consolidation zones

- Support and resistance levels

- Chart patterns

The premise is that tight ranges compress volatility, storing energy that releases as large directional moves once the price breaks free. Crypto frequently compresses before explosive moves, particularly around news events or liquidity shifts.

The strategy works best when:

- Low volatility suddenly expands

- High volume confirms the breakout

- Strong catalysts drive follow-through

The Order Flow Signature

False breakouts during thin liquidity destroy this approach. According to West Africa Trade Hub's analysis of Crypto trading strategies, breakout methods require careful confirmation to avoid getting trapped when the price reverses immediately after triggering entry signals. Without volume confirmation, breakouts often fail, leaving traders holding positions that move against them quickly.

3. Mean Reversion (Range-Bound Markets)

Mean reversion assumes that prices revert to their average after extreme moves.

Traders buy oversold conditions and sell overbought ones using indicators like:

- RSI

- Bollinger Bands

- Statistical deviations from moving averages

Range-Bound Resilience

Many Crypto assets oscillate within ranges for extended periods, creating predictable support and resistance zones. The strategy profits when prices bounce between boundaries with moderate volatility, allowing traders to repeatedly buy low and sell high within the established range.

Strong trends break mean reversion completely. When genuine directional moves emerge, prices can stay overbought or oversold far longer than seems rational. Traders who keep buying dips in a downtrend or selling rallies in an uptrend fight momentum until losses force capitulation.

4. Scalping (High-Liquidity, High-Activity Markets)

Scalping involves executing many trades per day to capture small price changes that last only seconds or minutes.

Success depends entirely on:

- Low fees

- Tight spreads

- Fast execution infrastructure

Slippage in Thin Markets

Crypto's 24/7 trading creates constant micro-movements, especially in major pairs with deep liquidity. The strategy works when spreads are tight, execution is instant, and transaction costs don't erase the small profits each trade generates.

Illiquid markets destroy the scalping edge. Slippage and wider spreads consume the tiny gains the strategy targets. One trader described watching their scalping system work beautifully on high-volume pairs, then collapse completely when applied to lower-cap tokens where execution quality degraded.

5. Swing Trading (Moderate Trends and Cycles)

Swing traders hold positions for days to weeks, capturing medium-term price moves within broader trends. This approach balances opportunity with time commitment, requiring less constant attention than scalping but more active management than long-term holding.

Identifying Support and Resistance Zones

Crypto markets often move in waves, with impulses followed by pullbacks. Swing trading profits from these cyclical movements when volatility is moderate, support and resistance zones are identifiable, and price action shows clear wave structure.

Extremely fast markets complete moves before swing entries trigger. When trends accelerate rapidly, the deliberate entry process swing traders use causes them to miss the bulk of the move or enter just as exhaustion sets in.

6. Arbitrage (Pricing Inefficiencies)

Arbitrage exploits price differences for the same asset across:

- Exchanges

- Between derivatives and spot markets

- Among related instruments.

Variants include:

- Spatial arbitrage (cross-exchange)

- Triangular arbitrage (currency pairs)

- Funding rate arbitrage (perpetual futures)

Market Microstructure and Lags

Crypto markets remain fragmented, with varying liquidity across platforms creating temporary pricing gaps.

The strategy works when:

- Price discrepancies are large enough to cover transfer fees and execution costs

- Capital is sufficient to make small percentage gains meaningful

- Transfer times are fast enough to capture the spread before it closes

Highly efficient markets close spreads instantly. As Crypto infrastructure matures, arbitrage opportunities shrink. What once offered consistent returns becomes a race against high-frequency systems with better execution speed.

Unified API Management

Traditional platforms make arbitrage unnecessarily difficult by forcing traders to:

- Maintain dozens of accounts

- Navigate endless verification hurdles

- Manually manage capital across disconnected exchanges

This fragmentation isn't just a hassle; it's a barrier to profitability.

Coincidence AI redefines the discovery-to-deployment cycle by consolidating execution across all major venues into one powerhouse interface. By providing unified liquidity access, the platform enables an AI Crypto trading bot to identify and close pricing inefficiencies the moment they appear.

7. Momentum Trading (High-Velocity Moves)

Momentum trading buys assets already moving strongly upward (or shorts those moving downward), expecting continuation rather than reversal. Unlike trend following, which waits for established trends, momentum trading focuses on shorter bursts of acceleration.

Momentum Oscillators (RSI and MACD)

FOMO, liquidations, and algorithmic flows can drive rapid price surges in Crypto. The strategy works during sudden volume spikes, news-driven moves, and periods of strong market sentiment when participation accelerates quickly.

Exhausted moves reverse suddenly. Momentum traders who enter late in a surge often find themselves holding positions just as buying pressure evaporates. Without clear exit rules, momentum trades can turn into unintended swing positions, leading to immediate drawdowns.

8. Market Making and Liquidity Provision (Neutral Markets)

Market makers place both buy and sell orders to capture the bid-ask spread rather than betting on direction. Some traders also earn exchange rebates or liquidity incentives for providing continuous two-sided quotes.

Bid-Ask Spread Decomposition

Every trade requires counterparties, allowing liquidity providers to profit from spreads without taking directional risk. The strategy works when prices are stable, trading volume is high, and spreads are wide enough to compensate for the risk of holding inventory.

Sharp directional moves cause inventory losses. When price gaps suddenly, market makers find themselves holding positions that move against them before they can adjust quotes. The spread they earned on previous trades is wiped out by a single volatile move.

9. Funding Rate and Basis Trading (Derivatives Markets)

This strategy targets predictable income from perpetual futures funding rates or differences between spot and futures prices. Traders typically hedge exposure to remain market-neutral, capturing the funding payment or basis differential without directional risk.

Delta-Neutral Portfolio Management

Perpetual contracts often pay recurring funding to balance long and short demand. When directional bias is strong in derivatives markets and funding rates are persistently positive or negative, the strategy generates consistent income regardless of price movement.

Rapid funding reversals or sudden price shocks break the hedge. When volatility spikes, the correlation between spot and futures can temporarily break down, leading to losses on one side of the position that exceed the funding income collected.

10. Event-Driven Trading (Catalyst-Driven Markets)

Event-driven strategies trade around specific catalysts, such as:

- Token launches

- Exchange listings

- Regulatory announcements

- Protocol upgrades

- Macroeconomic releases

The approach bets that new information will move prices predictably.

Crypto reacts quickly and dramatically to new information. The strategy works when events are clearly defined, attention is close, and narrative momentum is strong enough to drive follow-through after the catalyst.

Confirmation Bias in News Trading

“Buy the rumor, sell the news” reversals punish late entries. By the time an event occurs, much of the anticipated move has already happened. Traders who enter based on the event itself often find that the price peaks at the announcement and reverses immediately.

But knowing which strategy fits which market style is only half the equation. The harder truth is that most traders fail even when using objectively profitable approaches.

Related Reading

- What Is OTC Trading Crypto

- What Are Crypto Trading Signals

- Best App For Crypto Day Trading

- Best Crypto to Day Trade

- Best Crypto Copy Trading Platform

- Best Crypto Trading Tools

- Crypto Futures Trading for Beginners

- Crypto Day Trading Strategies

- Best Crypto Trading Platform

- Advanced Crypto Trading Strategies

Why Most Traders Fail Even With Profitable Strategies

A strategy can generate 40% annual returns in backtesting and still destroy accounts in live trading. The breakdown happens in the space between knowing what works and doing it repeatedly under stress. Most failures stem from execution gaps, not flawed logic.

Emotional Override Breaks the System

Rules collapse when losses trigger panic. Research from Daniel Kahneman and Amos Tversky on Prospect Theory shows people feel losses roughly twice as intensely as equivalent gains.

This asymmetry explains why traders exit winning positions after small profits but hold losing trades far past their stop-loss levels, hoping for a recovery.

Loss Aversion and the Pain Gap

After three consecutive losses, the strategy gets questioned. The rules that looked clear during calm markets suddenly feel unreliable. One trader described watching their P&L swing violently during a volatility spike, triggering emotions they didn't recognize.

The urge to override the system, skip the next signal, or modify position size becomes overwhelming. The strategy didn't fail. The ability to follow it did.

Quantifying Emotional Cost

DALBAR's Quantitative Analysis of Investor Behavior found that average equity fund investors consistently underperform the funds they own by several percentage points annually.

When the strategy needs them to stay committed, the gap comes from timing decisions driven by emotion:

- Buying after rallies

- Selling during drawdowns

- Abandoning positions exactly

Inconsistent Execution Destroys Statistical Edge

A profitable approach depends on playing out its statistical characteristics across many trades. Skipping signals because they “don't feel right” or adding discretionary entries that look compelling breaks the math that made the system work in testing.

The Cost of Filtering Signals

Strategy drift accelerates after losing streaks. Confidence evaporates, and suddenly the rules need “improvement.”

- Traders start filtering signals

- Adding confirmation requirements

- Reducing the size of setups that perfectly match their criteria

Trend-following systems often generate most of their annual returns from a handful of large winning trades. Missing even two or three of those trades while taking all the small losses eliminates profitability entirely.

Execution Algorithms (VWAP and TWAP)

Professional firms automate execution specifically to prevent this. When the signal triggers, the trade executes.

- No second-guessing

- No emotional filtering

- No selective rule-following based on recent results

Position Sizing Determines Survival

Entries matter less than how much you risk when wrong. A trader with accurate directional calls can still blow up if they size positions too aggressively. The math is brutal: a 50% loss requires a 100% gain just to recover. Three consecutive 30% losses reduce an account by 66%, requiring a 194% gain to break even.

The Anti-Martingale Approach

The European Securities and Markets Authority (2013) found that a majority of retail clients trading leveraged products such as CFDs lose money, primarily due to excessive leverage.

Crypto derivatives markets often allow this leverage:

- 20x

- 50x

- 100x

A 5% adverse move at 20x leverage wipes out the entire position. The strategy might be sound, but the position sizing makes survival impossible. Limiting risk to 1-2% per trade changes everything. Ten consecutive losses reduce the account by only 10-18%. Recovery becomes achievable rather than requiring a miracle performance.

Slippage and Execution Costs Erode Paper Profits

Backtests assume you get filled at the exact price you want. Real markets introduce friction. Spreads widen during volatility. Liquidity disappears when you need it most. Orders execute several ticks away from your intended price, especially in fast-moving conditions.

Redundancy and Multi-Venue Execution

During the March 2020 and May 2021 Crypto sell-offs, exchanges experienced outages and severe order delays. Traders watched prices collapse while unable to exit positions. Stop losses didn't trigger. Limit orders sat unfilled as price gapped through them. What should have been manageable losses became catastrophic because the infrastructure failed under stress.

High-frequency approaches like scalping are particularly vulnerable. A strategy earning 0.3% per trade becomes unprofitable once you account for 0.15% in combined fees and slippage. The edge exists only if execution quality remains pristine.

Eliminating the Latency Tax

Traditional workflows actively work against your profitability. Checking prices on one platform, verifying liquidity on another, and then manually placing orders introduces a “latency tax” that costs you money on every single trade.

Coincidence AI eliminates this friction by consolidating execution, unified liquidity access, and deep on-chain positioning data into a single, high-performance interface. By integrating these streams directly with an AI Crypto trading bot, the platform ensures that your strategy isn't just fast, it’s synchronized.

Overfitting Creates Illusions of Edge

Strategies optimized on historical data often fail in the future. The process is subtle. A trader tests hundreds of parameter combinations, looking for the settings that produced the best returns over the past two years. They find a configuration that would have generated 60% annually. It looks robust. It feels scientific.

But complex strategies tested across many variables can appear profitable purely by chance. Academic research on backtest overfitting demonstrates that the more parameters you test, the higher the probability of finding combinations that worked historically but have no predictive power going forward.

Walk-Forward Analysis (WFA)

The strategy isn't detecting real patterns. It's fitted to noise, random fluctuations that happened to align in the past but won't repeat. Professional systematic traders use out-of-sample testing and walk-forward analysis specifically to catch this.

They deliberately hold back data the model has never seen, then test whether the strategy still works. Most overfitted approaches collapse immediately.

Market Regimes Shift Without Warning

A strategy that thrives in trending markets suffers in consolidation. Mean reversion approaches profit during range-bound action but gets destroyed when genuine trends emerge. Low-volatility systems break during volatility spikes.

Narrative vs. Technical Flips

Crypto amplifies this problem. Liquidity cycles shift rapidly. Regulatory announcements change sentiment overnight. Narrative-driven flows create sudden regime changes that invalidate approaches that worked for months. A breakout system that captured three major moves in a row suddenly generates eight consecutive false signals as the market transitions from trending to choppy.

The strategy didn't stop working. The environment it was designed for disappeared. Traders who don't recognize regime changes keep applying the wrong tool to the wrong conditions, watching equity curves flatten or decline while convinced the method itself is broken.

Transaction Costs Compound Relentlessly

Every trade costs money. Exchange fees, bid-ask spreads, blockchain gas fees, and funding rates on perpetual futures all subtract from gross returns. For strategies with thin profit margins, costs can flip positive expectancy into negative. A scalping system that generates 50 trades per week with an average 0.4% gain per trade looks profitable until you include 0.2% in combined costs per round trip. Suddenly, half the gross profit disappears.

Over a year, that difference determines whether the account grows or slowly bleeds. High-frequency approaches require access to the lowest fee tiers to remain viable. Retail traders paying standard rates often can't profitably execute strategies that work for market makers with rebate structures.

The Discipline Gap

Two traders can use identical rules and produce opposite results. The difference isn't intelligence or market knowledge. It's the ability to execute consistently when markets become uncomfortable.

After a losing streak, one trader follows the next signal exactly as planned. The other skips it, convinced the strategy needs adjustment.

That skipped trade captures:

- A major move

- Recovers previous losses

- Generates significant profit

The trader who skipped it never sees that result. They're already testing a different approach, convinced their original system failed.

Sample Size and the Law of Large Numbers

The edge doesn't live in the rules alone. It lives in following them through drawdowns, boredom, and the constant noise of conflicting opinions telling you to do something different.

But knowing why traders fail doesn't answer the harder question: how do you know if your strategy actually has an edge before risking real capital?

How Professionals Validate Strategies Before Trading Them

Validation separates speculation from systematic trading. Professionals test strategies across historical data, forward market conditions, and multiple stress scenarios before risking capital. The process isn't about proving a strategy works once.

It's about confirming it survives:

- Different market regimes

- Transaction costs

- The psychological pressure of real execution

Backtesting Across Multiple Market Cycles

Programming Insider reports that 95% of professional traders backtest strategies across at least 3 years of historical data, specifically to capture different:

- Volatility regimes

- Liquidity conditions

- Trend characteristics

Testing only bull market periods creates blind spots. A strategy optimized on 2020-2021 data might show an 80% win rate but collapse during the 2022 bear market, when correlations shifted, and liquidity evaporated.

Risk-Adjusted Ratios (Sharpe vs. Sortino)

Professionals examine metrics beyond total return. Maximum drawdown reveals the worst peak-to-trough decline, helping you determine whether you could psychologically withstand that loss without abandoning the system.

Profit factor (gross profits divided by gross losses) shows whether winners meaningfully exceed losers. Trade frequency determines if the strategy generates enough opportunities to be statistically meaningful or relies on a handful of lucky trades.

Forward Testing in Live Market Conditions

Backtests simulate perfect information. Forward testing exposes how strategies perform when you don't know what happens next. According to Programming Insider, 78% of institutional traders use forward testing for 3-6 months before deploying real capital, specifically to identify how real-time price formation, actual spreads, and execution delays differ from historical simulations.

Paper trading during this phase reveals performance decay, the gap between theoretical and realized returns. A strategy might show an average profit of 0.5% per trade in backtesting, but only 0.2% in live conditions once slippage, partial fills, and timing delays are factored in. If costs consume more than half the expected edge, the strategy likely won't survive real deployment.

Out-of-Sample Testing to Prevent Overfitting

Professionals reserve data that the strategy has never seen during development. This unseen period, the out-of-sample window, tests whether the system captured genuine patterns or merely fit historical noise. If performance collapses on fresh data, the strategy is likely to have memorized past coincidences rather than identified durable market behavior.

Walk-forward analysis extends this concept. The process repeatedly optimizes parameters on a past window, tests them on the subsequent unseen period, then rolls forward. This simulates how a strategy would perform if recalibrated periodically in real time, adapting to changing conditions without future knowledge. Strategies that degrade rapidly in walk-forward tests won't survive actual deployment, where market structure evolves continuously.

Stress Testing Across Assets and Conditions

Robust strategies work across multiple instruments and timeframes, not just the single asset they were designed around. Professionals apply the same rules across different tokens, varying market caps, and both trending and ranging periods. A fragile system that profits only on one coin during a specific volatility regime will break when conditions shift.

Typical robustness checks include testing in bull, bear, and sideways markets separately. A mean-reversion approach might show strong overall returns but reveal that all profits came from range-bound periods, while trending markets generated consistent losses. That insight changes deployment decisions. You either add regime filters to avoid unfavorable conditions or accept that the strategy will underperform during certain cycles.

Modeling Realistic Transaction Costs

Academic studies of high-frequency trading consistently show that profitability is highly sensitive to fees. A scalping system earning 0.4% per trade becomes unprofitable once you include 0.15% in combined exchange fees, spreads, and blockchain gas costs. The edge existed only in simulation, where costs were ignored or underestimated.

Professionals model commissions, bid-ask spreads, market impact from order size, and funding rates for derivatives. They also account for the reality that liquidity disappears during volatility spikes, widening spreads exactly when you need to exit positions. A stop loss set at 2% below entry might be triggered at 2.5% or 3% during a flash crash, when order books thin out.

Cognitive Hurdles in Execution

Most validation failures trace back to this gap. The strategy looked profitable because testing assumed perfect execution at mid-market prices. Real trading introduces friction that erodes or eliminates theoretical edge.

But even strategies that pass every validation test still fail if you can't execute them consistently when markets turn uncomfortable.

How Coincidence AI Helps You Turn Any Strategy Into a Live Trading System

Validation alone doesn't execute trades. The bottleneck for most traders isn't a lack of a testable idea; it's a lack of the infrastructure to translate that idea into consistent, automated execution without writing code or managing data pipelines.

Coincidence AI compresses what typically requires programming expertise into a workflow built around plain English instructions.

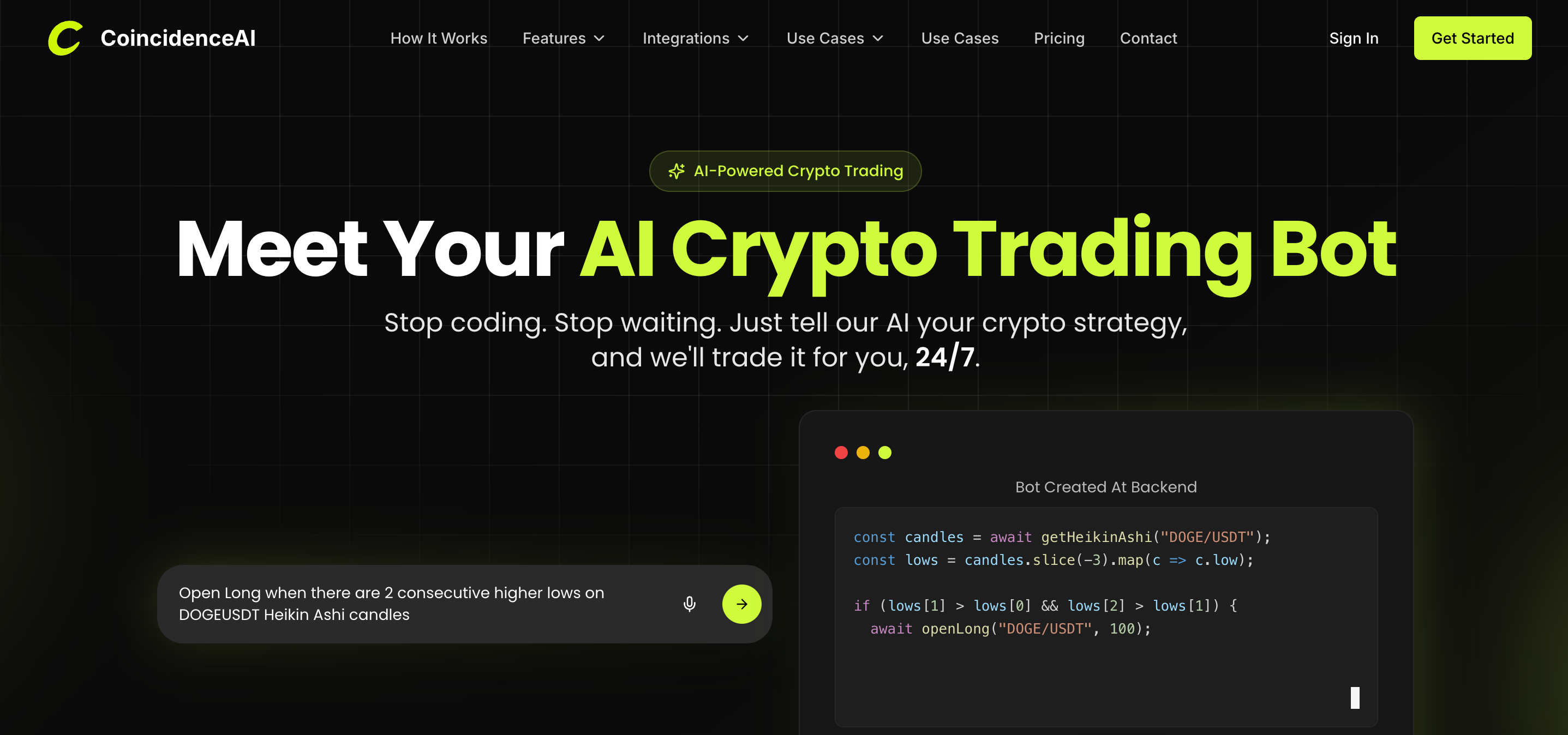

Describe Strategy Rules Without Coding

You specify conditions in natural language rather than syntax. “Buy when RSI drops below 30 and volume exceeds the 20-day average by 40%. Exit at 8% profit or 4% loss.” The platform interprets those parameters and converts them into executable logic that runs against historical price data.

This removes the barrier that prevents traders from understanding what they want to test, but from building the technical framework to validate it. No need to learn Python libraries, manage CSV files, or debug code when a backtest fails. The strategy exists as instructions, not scripts.

Instant Historical Validation

The system runs your rules against historical market data immediately, surfacing metrics such as win rate, maximum drawdown, profit factor, and average trade duration. You see whether the approach would have survived 2022's bear market or captured 2021's trending conditions before risking a single dollar.

Most retail traders skip this step entirely because manual backtesting feels prohibitively complex. They move straight from idea to live execution, discovering fatal flaws only after losses accumulate. Automated validation catches those flaws in minutes rather than months.

Live Deployment to Supported Exchanges

Once validated, the strategy is deployed directly to exchanges such as Bybit and KuCoin.

Orders execute automatically when:

- Conditions trigger

- Removing the risk of manual errors

- Missed signals

- Emotional interference

The system follows your rules exactly as specified, regardless of whether you're watching the screen or asleep.

According to Tickrad, AI-powered strategies are outperforming human-only methods specifically because automation eliminates the psychological friction that causes traders to override their own rules during volatile periods. When fear or greed would normally disrupt execution, the system continues operating according to plan.

Continuous Performance Tracking

Markets evolve. A strategy that worked beautifully during high volatility might degrade as conditions stabilize. Ongoing monitoring tracks live results against backtest expectations, revealing when performance diverges or when drawdowns exceed historical norms.

You can adjust parameters, pause deployment, or disable strategies entirely when real-world behavior no longer aligns with the tested assumptions. This closes the feedback loop that's typically missing in retail workflows, where traders often don't realize a strategy has stopped working until significant losses force them to recognize it.

Compressed Workflow From Concept to Execution

The process mirrors professional validation pipelines but removes the technical overhead.

Describe:

- The strategy

- Review backtest metrics

- Deploy live

- Monitor continuously

Each step occurs within the same interface, without switching between:

- Charting platforms

- Coding environments

- Exchange APIs

- Monitoring dashboards

Most retail traders attempt to cobble together this workflow using fragmented tools. They chart on TradingView, backtest manually in spreadsheets, execute on Binance, and track performance in separate journals. Every transition point introduces friction where strategies fail, not because the logic is flawed, but because execution becomes inconsistent.

The Unified Architecture of Coincidence AI

Coincidence AI consolidates:

- On-chain positioning data

- Real-time wallet tracking

- Breakout signals into a single, high-performance execution infrastructure

By integrating these critical streams, the platform compresses the discovery-to-deployment cycle, the exact window that determines whether your analytical edge survives its first contact with live markets.

When market regime shifts occur, the data revealing those changes appears exactly where your AI Crypto trading bot is already positioned to act. You no longer need to manually synthesize information scattered across dozens of browser tabs; the signal and the execution inhabit the same space.

Defining Statistical Significance

The emphasis isn't on predicting markets perfectly. It's about ensuring strategies run as designed, with measurable performance evidence across enough trades that statistical characteristics become visible. Consistency matters more than complexity.

But automation only works if you can actually describe what you want the system to do.

Trade With Plain English With our AI Crypto Trading Bot

Most traders don't need more indicators or strategy ideas. They need a reliable way to determine what actually works and to execute it without deviation.

The gap between knowing a strategy and running it consistently is where most edge disappears, not because the logic fails, but because:

- Manual execution introduces hesitation

- Second-guessing

- Selective rule-following that breaks statistical characteristics before they can materialize

Information Decay and Market Efficiency

Traditional workflows fragment the discovery-to-execution cycle across multiple platforms.

- You chart on one interface

- Validate ideas through spreadsheets

- Execute on exchanges with separate logins

- Track performance in disconnected journals

Each transition point introduces friction where strategies degrade. By the time you synthesize OnChain positioning data, wallet movements, and breakout signals from scattered sources, the opportunity has moved, or your conviction has weakened enough that you skip the trade entirely.

Integrated Intelligence: The Coincidence AI Ecosystem

Coincidence AI consolidates execution by:

- Providing unified access to on-chain analytics

- Deep wallet tracking

- Real-time social discovery within a single, high-performance interface

When market regime shifts occur or positioning data reveals hidden accumulation patterns, the information surfaces exactly where your AI Crypto trading bot is already positioned to act across tokens, perpetual futures, and prediction markets.

This architectural compression is vital; strategies succeed or fail based on your ability to act on high-fidelity signals without the costly latency introduced by manual synthesis across dozens of browser tabs.

Defining Statistical Significance

If you want to stop guessing which strategies might work and start trading based on tested evidence, Coincidence AI enables you to turn trading ideas into automated systems in minutes.

Describe:

- Your entry conditions

- Exit rules

- Position sizing in plain English

The platform validates those parameters against historical data, surfaces performance metrics, and deploys the strategy to live markets where it executes exactly as specified, regardless of whether fear or greed would normally override your discipline.

Start building your strategy with Coincidence AI today.